Accounting Standard Setting Has Been Characterized as

This has led the professionshow more content. Developing and publishing the exposure draft ED.

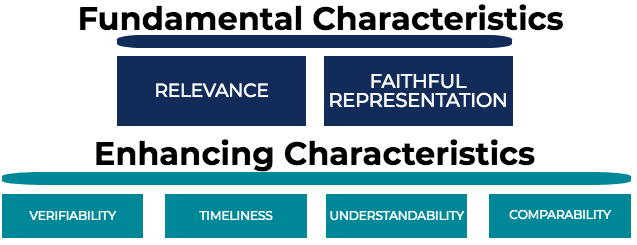

Qualitative Characteristics Of Accounting Information Overview Guide

Because the setting of standards is a social decision.

. 3 Pension plan accounting. Accounting standard setting has been characterized as. Using the scientific method.

Accounting for business combinations. The International Accounting Standards Board. This is a mandatory step.

Standards place restrictions on behaviour. Chapter 7 SHD. Accounting for postretirement benefits other than pensions.

With respect to the financial statements what is the value of an audit. Changes in standard can have significant impact on companies investors and creditors. Can overrule the FASB when their policies disagree.

The setting of accounting standards is as much a product of political action as of flawless logic or empirical findings. ACCOUNTING STANDARD SETTING. Accounting standard-setting has been characterized as.

Chapter 7 SHD. The process of setting accounting standards has been characterized as a political process. 8 accounting standard setting has been characterized.

Using the scientific method. Hence the process of setting accounting standards is a complex task. Accounting standard-setting has been characterized as a political process.

Using the scientific method. Failures to solve problem faced by practitioners accountant remains unresolved and lack of independence of financial information. 132Accounting standard-setting has been characterized as a political process.

Was the predecessor to the IASC. Accounting standard setting has been characterized as. Understand the standard-setting process.

2 The process of setting accounting standards has been characterized as a political process. Accounting standard setting is regulated because of the perception that the market is characterized by departures from the competitive ideal in ways that reduce benefits to society so the government intervenes to nurtures the public interest. This has led the professionshow more content.

Failures to solve problem faced by practitioners accountant remains unresolved and lack of independence of financial information. The standard setting process is a political process that is affected by the impact of several lobbying groups. Acceptance may be forced or voluntary or some of both.

Can overrule the FASB when their policies disagree. Therefore they must be accepted by the affected parties. Accounting Standard Setting pic Dont use plagiarized sources.

Evaluate this process citing an example. Expert Answer There are several groups that influence the standard setting process. Developing and publishing the standard.

133What are the key provisions of the Public Company Accounting Reform and Investor Protection Sarbanes-Oxley Act of 2002. Since 1960s accounting profession has been criticized for its weakness. General economic conditions are also considered in setting standards because these conditions affect the cost of materials.

Accounting standard-setting has been characterized as a political process. Usually effective standards are the result of engineering and time and motion studies undertaken to determine the amounts of materials labor and other services required to produce a product. Using the scientific method.

The International Accounting Standards Board. Discuss this proposition giving an example Changes in GAAP can have significant differential effects on companies investors creditors and other interest groups. What are the key provisions of the Public Company Accounting Reform and Investor Protection Sarbanes-Oxley Act of 2002.

Get Your Custom Essay on. 137 Accounting standard-setting has been characterized as a political process. ATPB 313 ACTB 423.

2 The process of setting accounting standards has been characterized as a political process. Since 1960s accounting profession has been criticized for its weakness. Discuss this proposition giving an example.

Accounting standard-setting has been characterized as. The process of setting accounting standards has been often considered as a political process. The IASB must issue an ED.

A change in accounting standard can have a huge redistribution of wealth in the economy. However this is not mandatory. Public-interest market failure theory.

Accounting standard setting has been characterized as A A political process B from ACG 4101 at Florida International University. The IASB may re-expose an ED particularly where there are major changes since the ED was first released in stage 4. Evaluate this process citing an example.

Was the predecessor to the IASC. The IASB may issue a discussion paper. 8 Accounting standard-setting has been characterized as.

ACCOUNTING STANDARD SETTING. Changes in GAAP can have significant differential effects on companies investors creditors and other interest groups. Accounting Theory Practice.

Discuss this proposition giving an example. The most recent example of the political process at work in standard-setting is the heated debate that occurred on the issue of. Three major categories of theories regulation.

Discuss this proposition giving an example. 134With respect to the financial statements what is the value of an audit. Since 1960s accounting profession has.

Accounting Principles Explanation Accountingcoach

Ifrs Our Structure

Accounting Standard Overview History Examples

/paper-with-title-international-financial-reporting-standards--ifrs---850740234-6e303822ed5e4800b523b0ac24db396c.jpg)

International Accounting Standards Ias

Comments

Post a Comment